A check endorsement is the process of signing the back of a check to authorize its transfer, deposit, or cashing. Endorsements serve as a legal way to acknowledge receipt of the check’s funds and can take several forms, including blank endorsements, restrictive endorsements, and third-party endorsements. While a blank endorsement simply allows anyone holding the check to cash it, a restrictive endorsement adds instructions, such as “For deposit only,” to limit how the check can be used. Third-party endorsements, in particular, allow the original payee to transfer the check to another person, which can be useful for payments, gifts, or delegating deposits. Understanding these types of endorsements is crucial because improper endorsements can lead to rejected deposits, bank delays, or even fraud.

Why You Might Need to Endorse a Check to Another Person

There are several practical situations where you might need to endorse a check to someone else. For example, if you receive a check for a joint expense, such as rent or a shared utility bill, you might want to transfer it directly to the person responsible for paying it. Similarly, parents may receive checks intended for their children, such as allowance, scholarship, or birthday funds, and may choose to endorse the check to their child so they can deposit it in their own account. Third-party endorsements make it possible to transfer funds securely without withdrawing cash, offering a convenient and traceable way to handle payments.

Another common scenario is when someone is unable to visit their bank in person. If the original payee is traveling or otherwise unavailable, endorsing the check to a trusted individual allows the funds to be deposited without delay. This can be especially useful for businesses, freelancers, or remote workers who rely on timely payments. While the process may seem simple, it’s important to recognize that banks often have strict rules regarding third-party endorsements to prevent fraud. Therefore, understanding when and why to use this method ensures that the transfer is both safe and effective.

Step-by-Step Process for Endorsing a Check

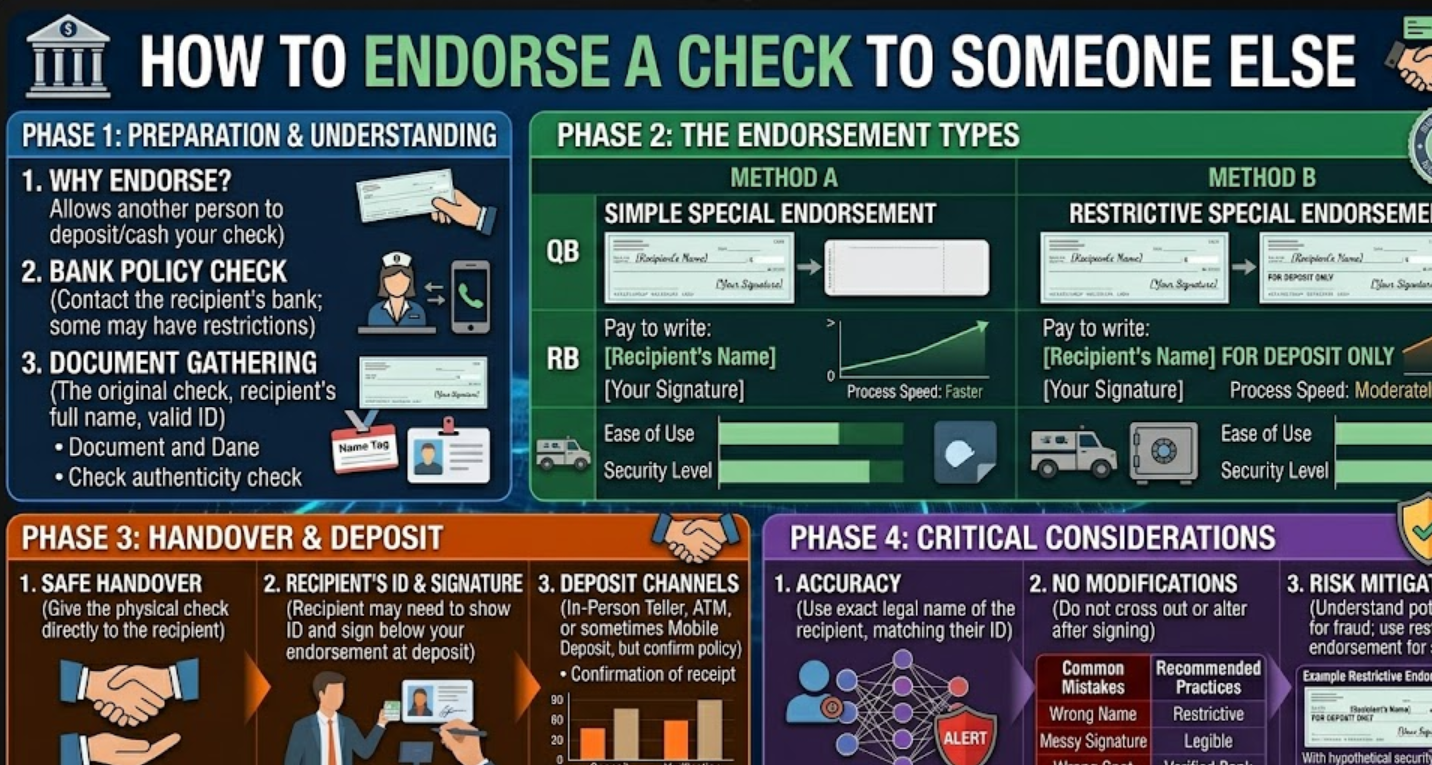

Endorsing a check to someone else involves a clear, careful process to ensure the transfer is valid and accepted by the bank. First, the original payee should verify with their bank that third-party endorsements are allowed, as some banks have strict policies. Next, the original payee signs the back of the check exactly as their name appears on the front, and directly underneath, writes the phrase “Pay to the order of [Recipient’s Name]” to officially authorize the transfer. After this, the new recipient should sign beneath the endorsement to confirm acceptance, creating a legally recognized chain of authorization. Finally, the recipient deposits or cashes the check at their bank, presenting valid identification if required. Following these steps carefully minimizes the risk of the check being rejected and ensures a smooth transaction for both parties.

Common Mistakes to Avoid When Endorsing a Check

One of the most common mistakes people make when endorsing a check to someone else is incorrectly signing or writing the endorsement. For instance, if the original payee misspells their name, leaves out the “Pay to the order of” phrase, or forgets to have the new recipient sign, the bank may reject the check. Another frequent error is using a check that has already expired or been damaged, which can delay processing or make the check completely invalid. Ensuring that the endorsement is clear, legible, and matches the names exactly as written on the front of the check is crucial to avoid these issues.

Another mistake is assuming all banks accept third-party checks. Some banks strictly prohibit them, while others require both parties to be present during the deposit. Additionally, some people overlook fraud risks, such as endorsing checks to someone they do not fully trust or leaving the endorsement blank, which can allow unauthorized cashing. To avoid these problems, always confirm the bank’s policies beforehand, use secure methods to transfer the check, and never leave blank endorsements. Small precautions can save time, prevent stress, and ensure that funds are safely received by the intended recipient.

Bank Policies and Legal Considerations

When endorsing a check to someone else, understanding bank policies and legal regulations is essential to avoid rejection or potential fraud. Many banks have strict rules regarding third-party endorsements and may require that both the original payee and the new recipient be present during deposit or cashing. Additionally, some banks only accept third-party checks if the funds are deposited into a personal account rather than withdrawn in cash. From a legal perspective, endorsing a check improperly can create liability if the check is lost, stolen, or fraudulently cashed. Always verify with your financial institution before transferring a check and keep a record of the endorsement to provide proof of authorization. Trusted sources like Chase Bank and Bank of America emphasize checking bank policies to ensure the transaction is valid and secure.

Tips for Safely Transferring a Check

Transferring a check to someone else requires caution to ensure the funds are received safely and without complications. One of the most important tips is to verify the recipient’s identity before endorsing the check. Only transfer checks to people you trust, as a lost or stolen third-party check can be difficult to recover. Additionally, avoid leaving the endorsement area blank, as this creates a risk that someone else could cash the check fraudulently. Using the proper endorsement format—signing your name followed by “Pay to the order of [Recipient’s Name]”—helps protect both parties and ensures the bank can process the check without issues.

Another key tip is to communicate with your bank before transferring a check. Some banks require that the new recipient present valid identification, and certain financial institutions may have restrictions on third-party checks. To minimize delays or rejected deposits, check with both your bank and the recipient’s bank about their specific requirements. Finally, consider keeping a record of the endorsement, including a photo of the check or a written note of the transaction. This documentation can be invaluable if questions arise regarding the transfer, providing proof that the funds were authorized to the intended person. Following these safety measures ensures a smooth and secure check transfer.

Alternatives to Endorsing a Check to Someone Else

Sometimes, endorsing a check to another person may not be the safest or most convenient option, and there are several alternatives that can achieve the same goal securely. For example, you can deposit the check into your own bank account and then transfer the funds electronically using services like Zelle, Venmo, or a direct bank transfer. Another option is to request that the payer issue a new check directly to the intended recipient, which eliminates the need for a third-party endorsement altogether. Some people also use mobile banking deposit options, where the original payee deposits the check via their bank’s mobile app and immediately transfers the funds digitally. These alternatives reduce the risk of fraud, avoid potential bank restrictions, and provide a faster, traceable way to get the funds to the right person.

Conclusion

Endorsing a check to someone else can be a practical way to transfer funds, but it requires careful attention to detail, bank policies, and safety measures. By understanding the process, using the proper endorsement format, and verifying both the recipient and your bank’s requirements, you can ensure a smooth and secure transaction. Remember, while third-party endorsements are legally valid, not all banks accept them, and mistakes can lead to rejected deposits or even potential fraud. For many, alternatives like electronic transfers or having the payer issue a new check directly can provide a safer and faster solution.

FAQs

1. Can anyone endorse a check to someone else?

Not necessarily. While most checks can be endorsed to another person, some banks have strict rules or may require both parties to be present. Always check with the bank first.

2. Is it safe to endorse a check to a friend or family member?

Yes, as long as you trust the recipient. Avoid endorsing checks to strangers or leaving endorsements blank to prevent fraud.

3. What happens if the bank rejects a third-party check?

If a bank rejects a third-party check, the recipient cannot deposit or cash it. In that case, the original payee may need to deposit it themselves or request a new check made directly to the recipient.

4. Are there safer alternatives to endorsing a check to someone else?

Yes. You can deposit the check into your own account and transfer funds electronically, or ask the payer to issue a new check directly to the intended recipient.

Visit for More Gossips and Information:- How Thread